Studies and experts alike agree that home staging is worth it, no matter what the market looks like.

While it’s true that in a seller’s market homes go quickly no matter what, the the housing market is slowly cooling. So, if you want to get top dollar for your home, home staging is worth the minor investment.

Additionally, if you want your home to stand out and receive the most and highest offers possible. Basically, you want buyers to fall in love with the home.

How does staging capture buyers’ hearts for a successful, top-dollar sale? Read on…

Home Staging is all about presenting the house as a warm, move-in ready home that ideally home buyers can visualize themselves in.

Update your décor with popular, on-trend style. Specifically, updates in living rooms, main bedrooms, and kitchens definitely make a positive impression. If homebuyers can start to see what it would look like to live in that home, they are likely to be more committed. They will also like be more willing to place a high offer. Moreover, if they can see themselves in the home, they are less likely to change their minds last minute or ask for a ton of concessions.

According to The National Association of Realtors®‘s 2021 Profile of Home Staging, 82% of buyers’ agents said home staging helped their clients visualize the property as their home.

Home Staging is Worth It.

Staging can minimize the negatives and accentuate the positives of a property. Basically, it will help your home make the best impression possible.

These simple updates will help buyers see the home’s unique features and increase the perceived value.

It’s no surprise that a cold, empty property will not get the same attention as one filled with stylish, warm furnishings and accessories. Home staging instantly creates a more inviting room. Additionally, homebuyers can get an idea of what kind of furniture would fit in the space.

Furthermore, you may only have one chance to catch the eye of homebuyers scrolling through hundreds of pictures online. Nearly all—99%—of millennial home buyers start their search online, according to NAR’s data. Even in a hot market, staging a property to look amazing in photos will draw more buyers to see the home in person and even submit an offer.

Lastly, staging is an investment which helps maximize the rate of return on the sale of the property. Cost to stage a vacant home can vary, typically less than or around $5000 and usually less than the first price reduction!

With an average investment of 1% of the sale price into staging, about 75% of sellers saw an ROI of 5% to 15% over asking price, according to data from the Real Estate Staging Association (RESA).

A recent survey from the International Association of Home Staging Professionals shows that staging helps sell homes three to 30x faster than the non-staged competition. Further, staging can help increase the sale price by up to 20% on average.

For those who decide not to stage, the average price reduction on a home was 5 to 20 times more than what it would have cost to stage the home. Not to mention the higher selling price they probably would have received as well.

All things considered, you can see that there is a strong argument that staging is worth the investment (which in perspective is a small one at that).

5/22/2022

For a list of luxury gated communities in Denver and the surrounding areas, look no further. Many of Denver’s exclusive and luxurious neighborhoods are gated communities.

However, for many who are looking for a luxury home, price alone is not enough. The neighborhood, its surroundings and privacy are usually key factors in considering whether or not a home has elite status.

Gated communities come in a few different varieties.

Many are simply automated, requiring a key card or transmitter for residents to enter. Visitors typically have a separate entry gate fitted with a kiosk that has a directory and pad for code entry. Most of these are also fitted with cameras for added security.

Additionally, some luxury neighborhoods have gate attendants that monitor the entrance and often take the name and driver’s license number of visitors for documentation before manually controlling the gate.

A few luxury communities in Denver and the surrounding areas are not physically surrounded by walls. However, there is a gate at entrances guarded by 24 hour security personnel. Specifically, Cherry Hills Farms and Cherry Hill Village are two prominent luxury neighborhoods with this type of security.

Tucked away right within the city limits of Denver, you will find:

Within Cherry Hills Village you have:

In the city of Greenwood Village:

The community of Highlands Ranch has:

The city of Parker has:

Within the city of Englewood there are:

The community of Littleton has:

Broomfield has:

The city of Lone Tree:

The area of Castle Pines and Castle Pines North:

Out west in the city of Morrison you will find:

The city Golden has:

Down south in Sedalia:

Up in the mountains within Evergreen:

If so, you’re not alone. It’s a question we get all the time in similar variations… “Are we in a housing bubble?”, “When is the housing bubble going to pop?”, on and on…

It’s a very valid question, especially for those of us who experienced, painfully, the housing market crash of 2008.

But it’s important to understand what led up to the housing crash of 2008 and what’s different today.

Homeownership has always been a cornerstone of the American Dream. Over 86% of Americans agree homeownership is a key part of the American Dream according to a recent report from the National Association of Realtors (NAR).

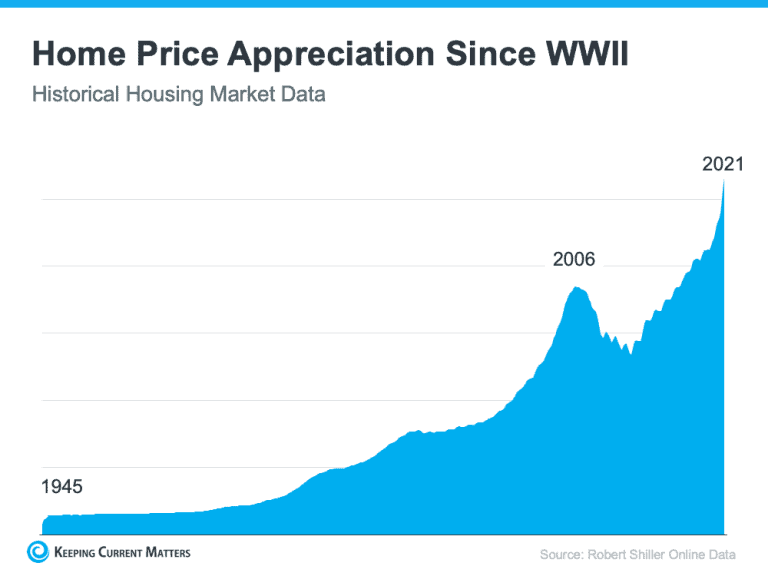

Before 1950, less than 50% of families owned their own homes but that soon changed with the GI Bill gave many of the returning veterans from WWII the ability to purchase a home. Since then homeownership moved upwards to 65% and the strong desire for owning your own home has continued to grow, helping home values to appreciate over the years.

As you can see, the only time home values dropped significantly since 1945 was during when the housing bubble of 2006-2008 popped. While some think the sharp increase in prices during 2006 looks very similar to the rise we’ve seen in the past 2 years and thus means a crash is coming, there are differences between the two periods of increases.

In 2006, homebuyers were not truly qualified for the mortgages they were given. Many could not afford to continue paying their mortgages and the market was flooded with foreclosures

⇒ Foreclosures caused a domino effect and banks along with the rest of the economy was in tailspin

⇒ Home values dropped…like off a cliff

⇒ some just walked away from their homes when they realized they owed more than what it was worth

⇒ more foreclosures ⇒ more decline in home values over the next few years.

2 Reasons today’s market is not like the one we experienced 15 years ago…

Prior to 2006, banks were creating artificial demand by lowering the standards needed to qualify for a home loan or refinance their current home – meaning even those with bad credit history, no stable income, etc… “qualified” for a loan. Today, regulations to prevent a repeat of 2006, require much higher standards to qualify for a loan – you really have to show that you’ll be very likely to make your payments.

For the last year or two, the demand for homeownership is a reaction to the recent COVID-19 world-wide pandemic that caused people to re-evaluate the importance of having a home. Lockdowns will do that! Plus remote work seems like it’s staying around to some degree, increasing the options for those who don’t have to live so close to work. It also increases the demand for a home that can double as an office so many people are looking to move out of their smaller, rented apartments onto a bigger house.

Rent is also going up so renters are now having the desire to build equity and stop giving money to a landlord also drives the demand for home buying.

When home prices were on a rapid incline in the early 2000s, many thought it would continue as such and so they started to borrow against the equity in their homes to finance college educations, new cars, boats, and you name it. However, when prices started to fall, many of these homeowners owed more than their house was now worth, causing some to just abandon their homes. This led to more foreclosures.

Homeowners haven’t forgotten the lessons of the housing crash even as prices have skyrocketed the last few years. Accessible home equity has more than doubled compared to 2006 ($4.6 trillion to $9.9 trillion) according to Black Knight.

The latest Homeowner Equity Insights report from CoreLogic reveals that the average homeowner gained $55,300 in home equity over the past year alone.

Today’s homeowners will not face an underwater situation even if prices dip slightly. Overall, homeowners today are much more cautious and there are regulations to make sure banks and others don’t get too greedy.

The housing market crash 15 years ago was due to a flood of foreclosures that was fueled by shady mortgage practices. No one wants that to happen again. Therefore, with the increased regulations, stricter mortgage standards and an increasing level of home equity, there is no realistic reason to believe that today’s housing market will crash.

You are not alone. According to Pew Research, the past two years saw the ranks of retirees 55 and older grow by 3.5 million!

Retirement, like other major events in life can have a huge impact on what you need from a home.

Retirement, or even semi-retirement is one of the biggest changes most of us will face in our lives. It’s often a period of time that most of us look forward to… more time to relax, travel, visit loved ones, enjoy hobbies, etc…

As we focus more on these important things in our lives we reconsider what we need from a home as well. Downsizing is typically appealing as the old adage of “Less is More” starts to ring true.

Most people of retirement age, usually those over age 55, choose to sell the homes they raised their children in and move into smaller more manageable homes so they have more time to spend visiting loved ones, traveling and/or doing other hobbies that take them out of the house.

Some may even move out of the area to be closer to loved ones or to an area they’ve always wanted to live in but couldn’t due to work or other restrictions.

Benefits of downsizing are numerous and often appealing to those who are looking forward to spending more time enjoying the precious things of life and less time in the rat race. Some pros of moving into a smaller home include:

The home equity you’ve built up in your existing house can be a huge help if you move. and move. According to the latest Homeowner Equity report from CoreLogic, the average homeowner in the US gained about $55,300 in equity over the last year.

Those equity gains can provide for a larger down payment, meaning smaller monthly mortgage payments which can often translate into more financial freedom. Having the funds from a recent home sale can also help you buy a house in this very competitive market, since offering more money up front helps your offer stand out.

Whatever your future home-owning experience entails, having a caring, knowledgeable realtor on your side can help you find what’s best for you in your current situation.

We, at The C. Taylor Group, can be the realtors you need in whatever stage of life you find yourself in. We understand the changes that occur in life and we want to do everything we can to reduce your stress during the home selling/buying process so that you can spend more time doing what’s important to you and enjoy all that life has to offer.

If you plan to retire soon or have already started enjoying retirement, you may be thinking of how you can adjust your housing requirements accordingly. Meaning now may be the perfect time to downsize. Let’s connect so we can work together to find a home that fits the needs of your current situation.

It’s a recurrent question in the mind of every renter as they see their rent continue to rise. Just in this last year, Colorado saw an increase of rental rates by almost 22% according to Rent.com. Their records show that in 2020, the average monthly rent for a one bedroom was $1,574. In 2021, according to their report, the average monthly rent for a one bedroom was $1,919.

And if you think rental prices will come down, don’t hold your breath. That just doesn’t really happen. According to nationwide Census data, rent has risen consistently for decades. Decades. They may not rise as quickly as they have recently, but they aren’t going down.

Buying a home is a major life decision and one that no one should enter into lightly. But at the rate rent is rising, it’s no wonder that we are getting so many renters wondering if now is the time to take the plunge into homeownership. I mean… having a stable monthly mortgage rate where you are actually investing in something that could bring you more money down the line, sounds really appealing in contrast to the steep increase in rent that is not likely to change anytime soon.

Of course, there’s no single correct answer for everyone. There are pros and cons to both renting and buying along with several factors that will help you know whether renting or buying a home is right for you right now.

If you’re on the fence about whether you should rent or buy, read on for:

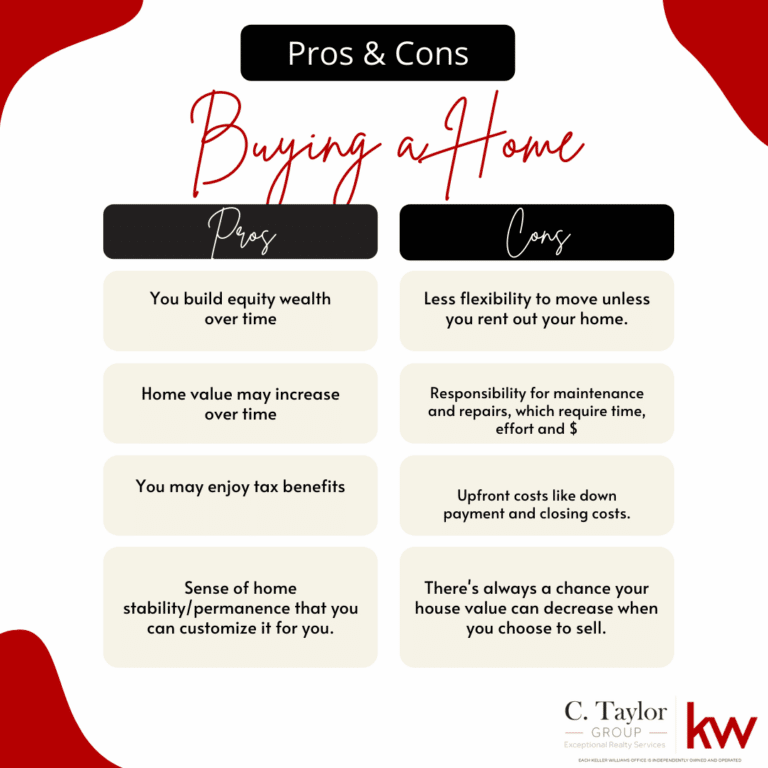

Do you thrive on being able to pick and relocate whenever you want or need to? Unless you’re good with owning a home and renting it out while you’re elsewhere, homeownership may not be right for you yet. However, if you’re looking around and thinking you might want to put some roots down and get more connected with a community, owning a home could make that happen. Owning a home and staying in it for at least five years can be good for you financially and emotionally – there’s just something about having a place to call “home” and make it all your own.

Rent is just a flat monthly rate that typically increases each year. As mentioned above, it has increased significantly over the last 1-2 years but typically it’s a more modest increase. However, it is an increase and the money each month is given to a landlord or property owner and you create no equity to capitalize on in the future.

Owning on the other hand, has quite a few more upfront costs such as a down payment, closing costs, and other miscellaneous home maintenance costs if needed. There are usually some other monthly fees that you may not typically see if you rent. These include property taxes, homeowners insurance and (in many cases) mortgage insurance as well as homeowners association (HOA) fees. If you’re getting financing for your home (i.e. a mortgage), you’ll likely have a set monthly payment that doesn’t increase for a set amount of time, usually 15-30 years.

All those costs can seem overwhelming but keep in mind that buying a home is almost always the better financial decision in the long run and most importantly, it will give you an opportunity to build equity – which in turn will help your credit and provide even more opportunities down the line. Remember also, each payment goes towards paying off the house and when you sell the house (for likely more than you bought it for) you will get to keep the money minus whatever is still owed on the house.

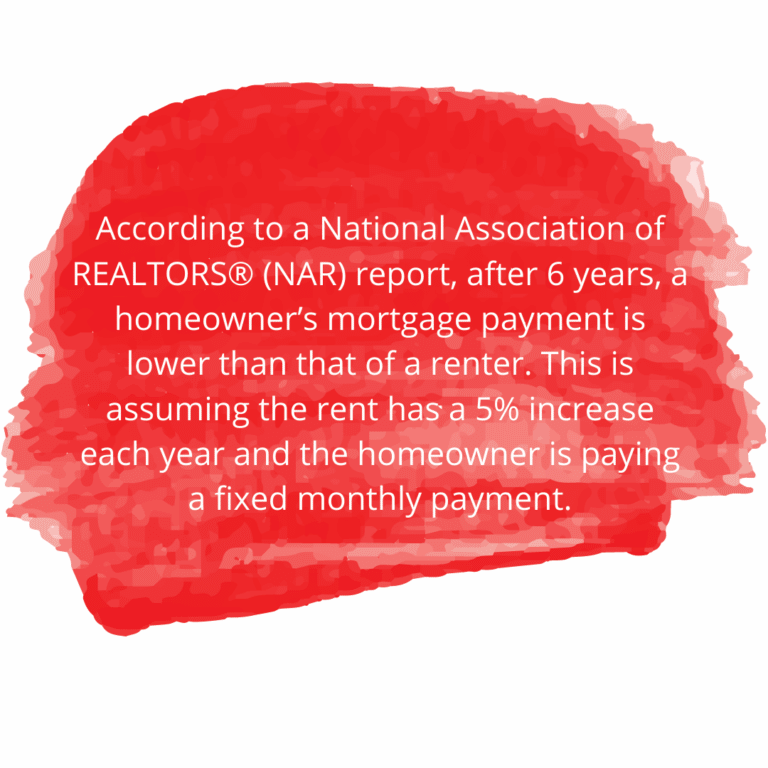

There are also tax savings to being a homeowner, especially if you are a first time home buyer. According to the same NAR report, a homeowner’s payment will be less than a renter’s payment after 3 years.

Even with meticulous planning, it’s hard to predict what can happen next in your life. But if you have some idea of where you’d like to be and do with yourself for the next 5-10 years, ask yourself does buying a home fit into that plan? For example, if you intend to stay put in one place for at least 5 years and have the financial means to do so, buying a home probably makes the most sense.

However, if your current life situation offers no hint of stability for the next few years and your housing needs might change, you may want to wait on buying a home. Plus it will give you time to figure out what you do want for the next few years and how to save up and prepare for possibly buying a home in the future.

Like with practically everything, there are risks for both renting and buying a home that you need to keep in mind. While it’s true, you can build equity when buying a home, it’s not a risk-free process. For example, because building equity takes time, if you sell your home sooner than planned, you may not recoup what you spent in closing costs or renovations when you first purchased the home.

And then there are the home maintenance costs. These are expenses you’ll need to pay to keep the home in top condition. Think winter maintenance, blowing out sprinklers, checking air filters and vents, testing fire alarms, landscaping and fixing plumbing issues, among other repairs that can pop up from time to time.

If you’re focused on other life goals, like a career that requires you to travel often, or if you have multiple young children to attend to, adding home maintenance to your list of responsibilities may not be the best choice. Some people love handy work around the home but if you have a career or a young family that needs a lot of your attention, you may want to reconsider owning a home unless, of course, you can pay someone else to do those things for you!

Last but definitely not least, is affordability. Can you afford to buy a house right now? When considering whether or not you should rent or buy a home now, it comes down to whether you can financially. We want you to understand all the pros and cons to home buying vs renting and you should be realistic about what you can and want to do.

You also need to take into consideration what the market is doing and what projections are for the near future if you decide to wait.

As we speak, here in 2022, the demand for housing is still very high and there are still relatively few houses up for sale. This means that house prices are high and while they may not rapidly increase like they did in the last 2 years, they will continue to go up for a while. The benefit to buying right now would be to take advantage of the relatively low mortgage rates and the fact that those are projected to increase. Wait too long though and increased home prices along with higher mortgage rates = higher monthly mortgage payments.

Other key factors that influence affordability include the location and the prices of other homes or rentals in the area you wish to live. You’ll also need to consider your credit score and if a lender would find you creditworthy unless you can pay cash upfront.

Once you’ve factored in the home’s purchase price, down payment and closing costs, as well as a monthly mortgage cost, compare that to the monthly cost of rent and projected costs over a period of time, say 5 years. With that comparison, you’ll be able to see the differences between costs as well as the perceived equity you would’ve built up in a home.

Either way, careful budgeting will help you succeed no matter what you choose, rent or buy.

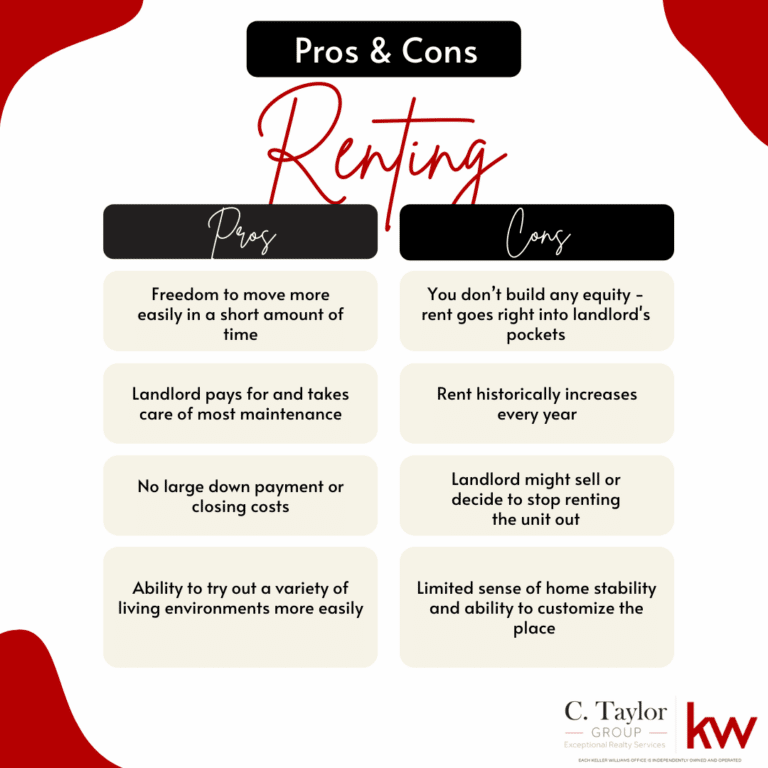

To Review: Here are some Pros & Cons to Renting and for Buying a Home

As you can see, there isn’t always a clear answer to the question of whether to rent or buy a home. A lot of factors go into making the decision and depending on your life situation and finances, the answer might change with time.

Homeownership has numerous benefits but if you’re on the fence, consider the pros and cons of each option. Renting may be what’s best for you right now but there are things to think about and we, at The C. Taylor Group, want you to be well informed.

Each LoKation office is independently owned and operated.

Privacy Policy | Copyright ©2022 C. Taylor Group. All Rights Reserved | Sitemap